Q4 2025 Market Commentary

2025 Market Recap

2025 was a year that tested investor expectations and ultimately rewarded discipline.

Beneath strong headline returns, 2025 proved to be a demanding and often counterintuitive year. Volatility driven by major policy shifts in tariffs, taxes, and immigration challenged sentiment. Nonetheless, markets continued to advance toward what may prove to be the most consequential technological transformation in decades, driven by the rapid adoption of artificial intelligence and the unprecedented supporting capital investment.

In April, the S&P 500 experienced one of its most significant two-day declines of the postwar era followed by one of its strongest single-day gains in decades. Periodic pullbacks reflected concerns around valuation, concentration, and the durability of AI-driven investment among mega-cap leaders. Growth slowed but avoided a hard landing, buoyed by resilient higher-income consumer spending and business investment focused on productivity-enhancing technologies.

At the same time, tariff-related pressures, slower job growth, and higher borrowing costs disproportionately affected lower- and middle-income households and rate-sensitive areas of the economy. These headwinds contrasted sharply with the resilience of higher-income consumers. The divergence reinforced a K-shaped growth dynamic across the economy.

For disciplined investors, 2025 was ultimately rewarding. The economic expansion entered its sixth year, the Federal Reserve resumed its easing cycle as labor market conditions softened, and corporate fundamentals remained resilient. The S&P 500 finished the year up approximately 18%, capping one of the strongest three-year runs in market history.[1] Companies at the center of the generative AI build-out became the largest in market capitalization in history.

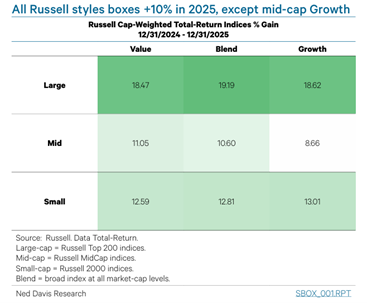

Importantly, 2025 defied the typical post-rally pattern of narrow leadership. Market participation broadened meaningfully across market capitalizations and sectors an encouraging signal for longer-term market durability.

International equities, long overshadowed by U.S. leadership, also contributed meaningfully. The MSCI ACWI rose more than 20%, supported by a weaker U.S. dollar, more attractive valuations, targeted fiscal stimulus abroad, and improving global manufacturing trends.[2] Performance broadened across Europe, emerging markets, and select Asian economies, reinforcing the benefits of global diversification.[3]

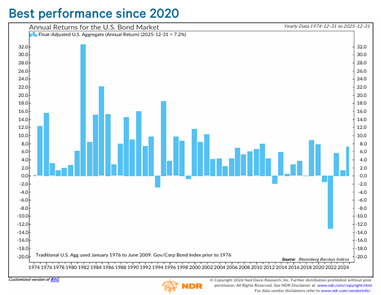

Fixed income delivered its strongest calendar-year performance in several years. The Bloomberg U.S. Aggregate Bond Index rose roughly 7%, supported by declining yields and the Federal Reserve’s pivot toward easing in the second half of the year. The 10-year U.S. Treasury yield peaked near 4.8% early in the year and ended around 4.2% despite elevated deficits and heavy issuance. For balanced portfolios, bonds once again provided both income and diversification benefits.[4]

Policy, Growth, and the Federal Reserve

U.S. GDP growth in 2025 stabilized in the 1.8%–2.0% range after recovering from early-year softness. Consumer spending and AI-related capital investment remained the primary drivers of growth, while exports and traditional manufacturing faced headwinds from tariffs and retaliatory measures. AI-related capital spending rose to a 4.5% share of GDP, exceeding levels seen at the peak of the dot-com bubble, highlighting both the scale of opportunity and elevated investor expectations.[5] The median institutional forecast calls for real GDP growth of 1.9%–2.2% in 2026, slightly below estimated potential, but consistent with continued economic expansion.[6]

Inflation moderated over the course of the year but remained uneven. Core inflation cooled sufficiently to allow the Federal Reserve to begin easing policy, though tariff pass-through effects became more evident in the second half. Services inflation eased more gradually as wage growth slowed and labor demand cooled with the unemployment rate drifting into the mid-4% range.

The Federal Reserve delivered three rate cuts lowering the federal funds rate to a target range of 3.5%–3.75%. While markets anticipate further easing in 2026, policymakers continue to emphasize data dependence, balancing lingering inflation risks against signs of cooling growth and employment.

Fiscal policy remained supportive but increasingly strained. Extensions of key tax provisions and targeted spending increases provided near-term support while intensifying concerns around deficits, rising interest costs, and long-term fiscal sustainability. Elevated Treasury issuance and a U.S. dollar that declined more than 10% during the year remain important macro considerations heading into 2026.[7]

Corporate Fundamentals, Valuations, and Sentiment

Corporate fundamentals remain generally healthy. According to FactSet estimates, S&P 500 earnings for 2026 are expected to grow approximately 15% year over year, marking a third consecutive year of double-digit growth. AI-related investment, productivity gains, and a resilient economic backdrop are expected to support results, with earnings growth gradually broadening beyond the technology sector.

Valuations remain elevated by historical standards. The S&P 500’s forward price-to-earnings ratio sits near cycle highs, reflecting optimism around AI-driven productivity gains and expectations for continued policy support. Valuations remain uneven, with mega-cap growth stocks trading at significant premiums while many cyclical, defensive, and international markets appear more reasonably priced.

Investor sentiment improved steadily throughout the year as inflation cooled and earnings proved resilient. Market breadth widened in the second half and major indices finished near record highs. That said, surveys of businesses and executives continue to reflect caution around hiring, capital investment, and ongoing trade policy uncertainty.

Positioning and Outlook

The past year reinforced the value of discipline, diversification, and opportunistic rebalancing. Throughout 2025, we maintained a modest overweight to equities, using periods of volatility to rebalance selectively rather than react to short-term headlines or market noise.

As we enter 2026, the investment backdrop remains constructive but increasingly nuanced. Trade policy uncertainty, inflation dynamics, uneven economic growth, and fiscal pressures present key risks. At the same time, powerful secular forces including AI adoption, productivity enhancement, infrastructure investment, and a more accommodative monetary policy continue to provide meaningful long-term tailwinds.

Within equities, we continue to favor U.S. markets supported by leadership in innovation and strong corporate profitability, while emphasizing diversification beyond the largest technology companies. International equities remain an important complement, benefiting from more attractive valuations, improving earnings trends, and the potential tailwind of a weaker U.S. dollar.

In fixed income, we maintain a modest tilt toward longer duration, positioning portfolios to benefit if interest rates ease as economic growth continues to moderate. We are also emphasizing high-quality bonds and liquidity within credit, as tighter spreads offer less compensation for taking additional risk than earlier in the cycle.

Our approach remains unchanged and aligned with clients’ long-term objectives: stay disciplined, remain diversified, and let data, not headlines, drive decisions. Periods of uncertainty often create opportunity, and we believe patient investors will be well positioned in the years ahead.

As always, we welcome your questions and look forward to discussing how this evolving environment may impact your portfolio. Thank you for your continued partnership and trust as we enter the new year.

[1] Morningstar Direct

[2] Morningstar Direct

[3] Morningstar Direct

[4] Morningstar Direct

[5] Ned Davis Research

[6] St. Louis Fed

[7]Ned Davis Research