Q3 2025 Market Commentary

The third quarter unfolded amid ongoing policy turbulence, with tariffs adding inflationary pressures and trade tensions persisting under the Trump administration. The U.S. economy remained resilient—supported by robust consumer spending and AI-driven investment—but faced headwinds from lingering supply chain frictions, moderating job growth, and elevated uncertainty.

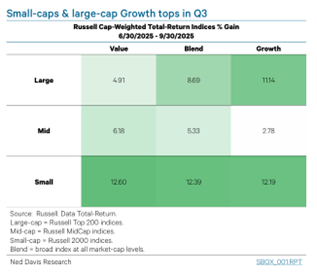

Despite these crosscurrents, equity markets climbed a wall of worry, extending their rebound with notable strength. The S&P 500 posted its strongest third-quarter performance since 2020, rising 8.1% and gaining roughly 14.8% year-to-date.[1] Quarterly gains were propelled by AI beneficiaries, positive earnings surprises, and growing expectations for Federal Reserve easing. Technology led the advance, while participation broadened as volatility fell to multi-year lows. As a result, small-cap stocks outperformed, rallying more than 12% during the quarter.[2]

International equities also delivered solid gains. The MSCI ACWI rose 7.6%, with 40 of 47 constituent markets advancing—led by emerging markets.[3] A softer U.S. dollar, targeted regional stimulus, and improving global macro momentum supported returns across Europe, Asia, and developing economies, even as trade retaliation and slower growth tempered enthusiasm.

Fixed income markets benefited from expectations of rate cuts and declining yields, though tariff-driven inflation concerns limited gains. The Bloomberg U.S. Aggregate Bond Index returned +1.1% in Q3, supported by a shift toward a more neutral monetary policy stance.[4]

Policy, Growth & Fed Outlook

U.S. GDP forecasts for 2025 have stabilized near 1.7%, reflecting a rebound from early-year weakness offset by tariff pressures on trade and investment. The Philadelphia Fed’s Q3 survey projects annualized third-quarter growth near 3.8%, driven by consumer spending and AI-related capital investment.

Inflation remains central to the outlook. Tariff passthrough has accelerated modestly, though core measures have cooled enough to permit monetary easing. The unemployment rate ticked up to 4.3% in August as payroll growth slowed but remained positive signaling a soft but stable labor market.

The Fed delivered its first rate cut since March 2024 with a 25-basis-point reduction in September, lowering the funds rate to 4.00%–4.25% and marking the start of a potential easing cycle after an 18-month pause. Markets are now pricing in two additional cuts this year amid balanced risks to employment and inflation. While expectations have shifted toward further easing, Fed officials continue to emphasize the need for clearer evidence of labor market weakness or sustained disinflation before acting more aggressively.

Despite a brief summer rally, the U.S. dollar remains down more than 10% year-to-date, pressured by high starting valuations, fiscal sustainability concerns, foreign concentration in U.S. assets, and questions about the durability of growth. [5] As the Fed pivots toward a more accommodative stance relative to other major central banks, narrowing interest rate differentials—combined with a persistent trade deficit—are likely to maintain downward pressure on the dollar.

Corporate fundamentals remain healthy. FactSet projects 9% S&P 500 earnings growth for 2025, with Q3 tracking near 8%, supported by resilient tech profits and buybacks despite modest margin compression from tariffs. Fiscal policy also remains a key variable. The administration’s “One Big Beautiful Bill”—a sweeping package of tax and spending measures—continues to shape growth expectations, deficit dynamics, and investor sentiment.

U.S. equity valuations remain historically elevated, supported by resilient earnings and optimism surrounding artificial intelligence and productivity gains. The S&P 500’s forward P/E ratio hovers near cycle highs, reflecting expectations for steady growth and policy support. However, valuations remain uneven—mega-cap technology companies trade at substantial premiums while many other sectors appear more reasonably priced. With sentiment and thematic momentum still dominant, sustained earnings growth will be critical to justify current multiples, particularly if the Fed’s move toward a more accommodative stance is delayed.

Sentiment and Technicals

Investor sentiment strengthened through the quarter, supported by broader market participation, new highs across major indices, and renewed fund inflows. AI-driven optimism and consistent earnings beats outweighed tariff concerns, though CEO surveys still indicate caution around future capital investment.

The volatility episode in April–May is now viewed as a healthy reset. Market breadth has since widened, and technical conditions remain supportive into year-end. Seasonally, the fourth quarter tends to favor gains, buoyed by easing financial conditions and improving investor confidence.

Positioning and Outlook

Staying Disciplined, Embracing Optionality

The calm advance in the third-quarter reinforced the importance of discipline and opportunistic rebalancing. We maintain a modest overweight to equities as we enter the fourth quarter.

Within equities, we continue to favor the U.S., supported by strong innovation, resilient corporate profitability, and healthy balance sheets. International markets also offer selective opportunities. Even after this year’s rally, valuations abroad remain attractive, trading at meaningful discounts to U.S. equities. With the dollar likely to weaken further—and U.S. investors still structurally overweight domestic markets—international equities appear well positioned to extend their relative strength.

In fixed income, we retain a modest duration bias to capture potential yield compression if growth weakens, while preserving ballast against equity volatility. Within credit, we continue to lean toward higher-quality corporates, balancing income with capital preservation.

Looking Ahead: Fiscal Tailwinds, Trade Headwinds

As we enter the fourth quarter, markets have become more adept at distinguishing policy noise from structural fundamentals. The outlook hinges on three key pivots:

· Tariff escalation remains contained.

· Inflation surprises stay benign or trend lower.

· Growth does not weaken materially.

The Trump administration’s protectionist agenda continues to reshape global trade. Key developments include:

· Fiscal Expansion and Easing: Tax permanency and spending under the “One Big Beautiful Bill” provide cyclical support alongside monetary easing.

· Tariff Escalation: Broad-based 10% duties—and targeted increases to 50% on metals and autos—have prompted retaliation and export softness yet are intended to bolster domestic production and supply-chain resilience.

· Deregulation: Rollbacks in energy and finance are supporting new investment commitments.

· Trade Retaliation: Countermeasures from trading partners and pending legal challenges add uncertainty.

These policies inject volatility but also create opportunity, particularly if accompanied by sustained monetary easing. While tariffs pose inflationary risks and may weigh on global trade, domestic sectors tied to infrastructure, reshoring, and AI investment could be relative beneficiaries.

If markets continue to separate short-term policy noise from long-term fundamentals, this late-cycle phase should support further equity gains—though with heightened volatility. Our positioning remains grounded in discipline, diversification, and long-term perspective, anchored in fundamentals rather than headlines.

As always, we welcome your questions and look forward to discussing how this evolving policy landscape may affect your portfolio.

[1] Morningstar Direct

[2] Morningstar Direct

[3] Ned Davis Research

[4] Morningstar Direct

[5] Morningstar Direct